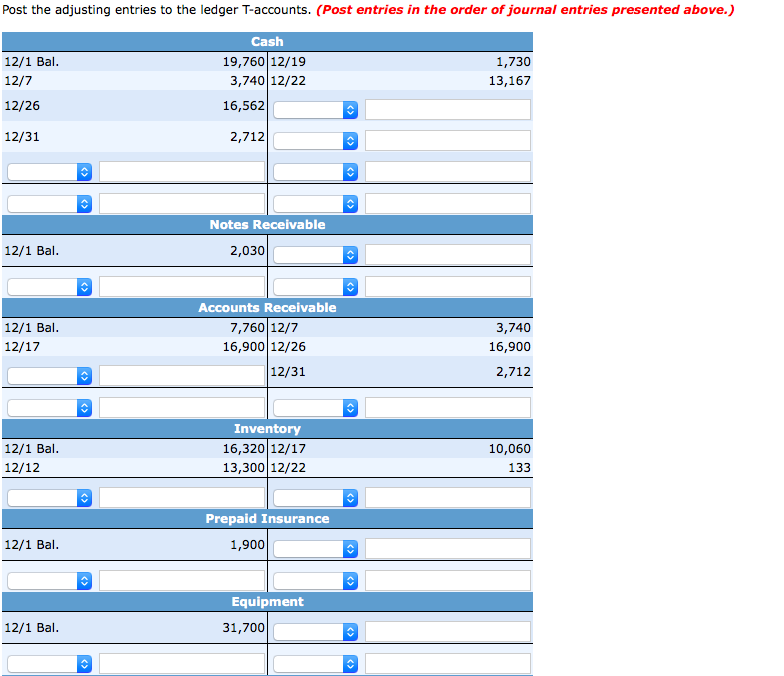

How to Make Adjusting Entries

Let’s explore how accrued vacation affects both the balance sheet and the income statement. Prepaid expenses or unearned revenues – Prepaid expenses are goods or services that have been paid for by a company but have not been consumed yet. This means the company pays for the insurance but doesn’t actually get the full benefit of the insurance contract until the end of the six-month period.

Do you own a business?

The construction company will need to do an adjusting journal entry at the end of each of the months to recognize revenue for 1/6 of the amount that will be invoiced at the six-month point. While unlimited vacation policies might seem cost-effective due to the absence of accrued liabilities, it’s important to remember that employees are still entitled to time off. The lack of a formal accrual system shouldn’t obscure the company’s responsibility to provide adequate rest and recovery for its employees.

What accounts are affected by an adjusting entry?

- For example, if you have an annual loan interest payment due in February and no liability is reflected on the books in January, you’re going to overestimate your available cash.

- The main objective of maintaining the accounts of a business is to ascertain the net results after a certain period, usually at the end of a trading period.

- Adjustment entries are made at the end of an accounting period, which can impact the timing of when revenue and expenses are recorded.

- When you make an adjusting entry, you’re making sure the activities of your business are recorded accurately in time.

- Adjusting entries are a crucial part of the accounting process and are usually made on the last day of an accounting period.

- Clear communication with your employees about vacation policies is just as important as accurate accounting.

For example, if a company has an account receivable that is unlikely to be collected, an adjustment entry is made to reduce the value of the asset. Similarly, if a company has a liability that has increased in value, an adjustment entry is made to reflect this change. Depreciation expense is the allocation of the cost of a long-term asset over its useful life. To record depreciation expense, an accountant would debit an expense account and credit an accumulated depreciation account.

Top 3 Examples of Adjusting Entries

The following Adjusting Entries examples outline the most common Adjusting Entries. Using an incorrect accrual rate or failing to account for nuances like part-time employees or varying work schedules can lead to significant discrepancies. For example, accruing vacation time based on hours worked is a common approach that promotes fairness, especially in businesses with fluctuating hours. However, if this method isn’t implemented correctly, employees might accrue less vacation time than they’ve earned. Unclear vacation policies can also create confusion and disputes, potentially impacting employee morale and productivity. A well-defined policy clearly outlining accrual rates, eligibility criteria, and carryover rules is essential.

Step 4: Make Adjusting Journal Entries

Entries are made with the matching principle to match revenue and expenses in the period in which they occur. Adjustments reflected in the journals are carried over to the account ledgers and accounting worksheet in the next accounting cycle. When you make an adjusting entry, you’re making sure the activities of your business are recorded accurately in time. If you don’t make adjusting entries, your xero service books will show you paying for expenses before they’re actually incurred, or collecting unearned revenue before you can actually use the money. It is impossible to provide a complete set of examples that address every variation in every situation since there are hundreds of such Adjusting Entries. The article will discuss a series of examples to understand better the necessity of adjusting entries.

The Importance of Adjusting Entries

With this method, vacation time is earned based on the number of hours worked, making it particularly useful for businesses with varying schedules. This approach ensures fairness by directly linking vacation time to actual hours worked. For example, an employee might accrue 1.5 hours of vacation for every 40 hours worked. For more information on managing vacation accrual methods, check out this guide. Overall, adjustment entries play a crucial role in ensuring the accuracy and reliability of financial statements.

Staying informed about the specific regulations in the states where your employees work is essential for accurate accounting and compliance. Check your state’s Department of Labor website or consult with legal counsel specializing in employment law for more information. Understanding both FASB guidelines and state-specific rules is crucial for accurate and compliant accounting for accrued vacation. This ensures your financial records reflect the true cost of employee vacation time and keeps your business legally sound.

An adjusting journal entry for an accrued expense will involve different accounts than one for accrued income, for example. Deferrals refer to revenues and expenses that have been received or paid in advance, respectively, and have been recorded, but have not yet been earned or used. Unearned revenue, for instance, accounts for money received for goods not yet delivered. The Financial Accounting Standards Board (FASB) provides generally accepted accounting principles (GAAP) that guide accounting practices in the US. Specifically, ASC 710, Compensation—General, addresses compensated absences, including accrued vacation. You can find detailed information on ASC 710 on the FASB website and other reputable accounting resources online.